10 reasons why the HDB Financial Services Ltd. IPO price band is relevant today while unlisted price is not…

Published on Sunday, June 22, 2025 by Chittorgarh.com Team | Modified on Thursday, November 6, 2025

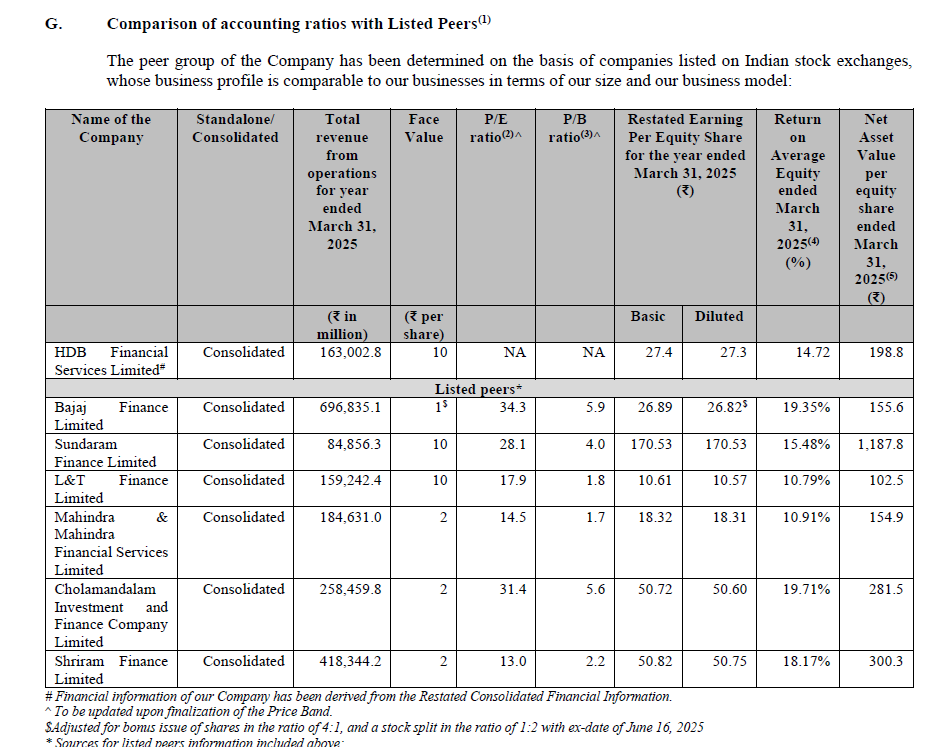

HDBF is the lowest Price/Book NBFC buy (calculated on upper end of the price band) as of FY25 (3.72 as NAV was Rs. 198.8)

IPO Price was revealed only on 20th June 2025 after getting due approvals. Since the IPO price is at 40% discount to unlisted price, this benefit is available to 1 crore active retail investors and 18.5 crore demat account holders. The number of Unlisted buyers are just 50,000 and they have invested in unofficial market at a time when the market was at a different high. Mostly these are HNIs who were chasing the stock in bull market peak.

HDFC Group cos have always rewarded shareholders and HDBF enjoys highest credit rating (CRISIL AAA/Stable and CARE AAA/Stable ratings) and investor confidence and demand for its debt instruments NCDs.

HDB Financial maintained robust double digit CAGR in its diversified granular loan book. HDB Financial has maintained Its Loan Book growth at robust 21% CAGR over the previous 2 years FY22–FY24 stands at a healthy 21.29%, showing robust and consistent expansion

HDBF's Provision Coverage Ratio (PCR) is highest among peers. As of FY24, HDBF’s PCR stood at 66.82%, showcasing prudent provisioning and a conservative risk approach --- significantly higher than many of its leading NBFC peers

HDBF maintains strong capital buffer and not raised any equity in last 7 years. HDBF had CRAR above 19% for 3 years. Capital Adequacy Ratio has consistently remained above regulatory minimums, with: FY22 – 20.22%; FY23 – 20.05%; FY24 – 19.25%; H1FY25 – 19.30%. This reflects HDB’s commitment to financial strength and regulatory compliance. HDB has not raised fresh equity since 2017, yet scaled its business through strong internal accruals and debt—uncommon for fast-growing NBFCs.

Robust branch expansion led to 1,772 branches across 1162 towns (outside top 20 cities). They show high branch efficiency and productivity to tap Rural, MSME Micro Ticket loan demand. HDBF has 80% branches outside top 20 cities. Branch Network expanded by 398 in 2.5 years.

NBFCs taking higher share from banks. Credit Market seeing a significant shift as NBFCs take higher share from Banks. NBFCs have expanding market share from 12% in FY08 to 20% in FY24. HDB, so far with its AUM, credit and profit growth outpacing its peers, has played a key role. HDB Financial is expected to be a significant beneficiary of the growing trend where NBFC are increasing grabbing share of the credit market away from banks

Strong Return Ratios and Asset quality: HDBF has Debt-to-Equity Ratio at 5.93x --- enabling higher returns while staying within Regulatory limits. Despite high leverage, HDB maintains strong return ratios and asset quality.

HDBF has access to funds at just 7.53% cost, which is one of the lowest among NBFCs. HDBF has access to diverse and competitive funding: HDBF has been able to raise funds from a wide range of domestic and global lenders (banks, mutual funds, insurance companies, etc.